She wakes up before everyone else. She makes the lunches, pays attention to the school fees, manages the household budget in her head like a silent, running spreadsheet. She may live with her in-laws, her parents, or entirely on her own. She may be widowed, divorced, or simply unmarried and navigating a world that wasn’t designed to support her independence.

She is the Indian woman in 2026. And the numbers tell her story better than any speech ever could.

This Women’s Day, we are not just celebrating strength — we are confronting reality. Because real empowerment begins with honest conversation. Especially about money.

The Numbers That Should Make Us All Stop

These are not abstract figures. These are women in your building, your mohalla, your family. These are mothers, daughters, and daughters-in-law who are managing the emotional weight of entire households — while often having no financial say in them.

The Single Mother: Carrying the World with No Safety Net

Let’s start with the woman who perhaps carries the heaviest load of all.

Single motherhood in India arrives through many doors — divorce, separation, widowhood, domestic violence, or simply the courage to choose independence. And when she walks through that door, she walks into a world that is deeply unprepared to receive her.

“There are those times when you wish there would be someone to help you share your load, take care of your kid, give you a break. That emotional drain you face of handling everything — finances, their education, household — all by yourself, takes a huge emotional toll.”— Beena Babu, Single Mother, Mumbai

What Beena describes is not weakness — it is arithmetic. One income. One decision-maker. Double the responsibility. Zero backup.

What She Faces, Financially

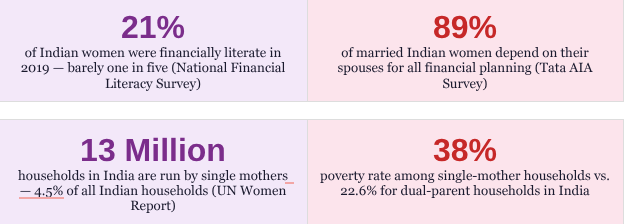

- Only 26% of single mothers in India receive an independent income — the majority remain financially dependent on extended family or male relatives (UN Women)

- Single-mother households face a poverty rate of 38%, compared to 22.6% for dual-parent households

- 82% of children raised by single mothers in India reported taking on financial responsibilities at a very young age, including working part-time to support their mothers

- Social stigma around single motherhood — especially in T2 and T3 cities — often limits her access to rental housing, credit, and even employment opportunities

What She Actually Needs

She does not need pity. She needs a bank account in her own name. She needs to understand SIPs, emergency funds, and term insurance. She needs to know her legal rights to maintenance and property. She needs a community of women who see her, not as a cautionary tale, but as a warrior deserving of practical tools.

The Daughter-in-Law: Last One to Know About Family Finances

She probably runs the household. She tracks the kirana budget, pays the school fees on time, and knows exactly which month the car insurance is due. But when it comes to the family’s investments, the FDs, the property documents — she is likely the last to know.

This is the paradox of Indian married women. She is trusted with the running of the home but excluded from its financial architecture. Her name may not appear on the property. She may not know the PIN of the joint account. She may have quietly handed over control of her own salary to her husband or in-laws without ever examining whether this was a choice — or simply what was expected.

The Joint Family Financial Dilemma

Living in a joint family has real advantages — shared childcare, emotional support, reduced living costs. But it also comes with financial vulnerabilities that are rarely talked about:

- Women in joint families often have no personal savings of their own — every rupee goes into a shared pool they do not control

- When marriages break down, women who managed joint family finances discover they have no documented financial assets in their name

- Financial decisions — from buying a car to booking a holiday — are often made without her input, even though she manages the day-to-day money

- Only 29% of Indian women have their own health insurance — in joint families, women are often assumed to be covered by a family policy they have never read

“For years, I felt like I didn’t have a voice in my financial decisions. Thanks to learning about healthy money relationships, I now look forward to being more proactive about my financial decisions.”— Archie Das, Architect

What Changes Everything

The single most powerful shift a woman in a joint family can make is this: open a personal savings account. Not a secret account — a personal one. Know your household’s financial position. Ask to be included in conversations about investments, insurance, and property. This is not distrust — this is self-respect.

The Woman Living with Her Parents: The ‘Waiting’ Trap

She might be in her late twenties or early thirties. She lives with her parents — either because she is unmarried, or because she returned home after a divorce or a difficult marriage. Society has a name for her situation. She has learned to ignore that name.

But here is the financial pattern that often follows: she earns, she contributes to the household, and she waits. She waits for marriage. She waits to ‘settle down’. And in the waiting, she does not invest. She does not build her own credit profile. She does not take out insurance. Because somehow, those things feel like they belong to a ‘real’ life that has not started yet.

The Cost of Waiting

Every year of financial inaction has a compounding cost. A woman who begins investing ₹5,000/month at 28 versus 35 will accumulate approximately ₹1.3 crore more by retirement, assuming a 12% annual return. The cost of waiting just seven years is not ₹4.2 lakh in foregone investment — it is ₹1.3 crore in foregone wealth.

And yet, the woman living with her parents often does not see herself as someone whose financial future needs building — right now. This is the quiet tragedy of the waiting trap.

What Does She Need?

- Your financial independence does not begin on your wedding day.

- Your parents’ home is not a reason to delay your financial growth — it is a gift of low overhead that makes building wealth easier.

- Every rupee you invest in your own name, every SIP you start today, every credit card you manage well — it all belongs to you. Regardless of what comes next.

- Start your emergency fund. Start your SIP. Get your own health insurance. Not later. Now.

The Working Woman: Earning More, But Still Not Free

India’s female labour force participation rate rose from 49.8% in 2017-18 to 60.1% in 2023-24 — a remarkable shift. Women are in boardrooms, startups, and classrooms in greater numbers than ever before. And yet:

The problem is not income. It is confidence — and the culture around it. Most women were raised in homes where money was either a taboo topic or a male domain. Even highly educated, professionally successful women often feel a deep-seated hesitation when it comes to investing, negotiating, or asserting financial preferences.

“Women are not risk-averse — they are risk-conscious. They want to invest, but they want to get it right.”— Outlook Money Survey, 2025

This is not a flaw. It is an orientation that, when supported with the right financial education, produces some of the most disciplined and thoughtful investors. The gap is not capability — it is a confidence one. And confidence is built through knowledge, community, and practice.

The Green Shoots of Change

There is real reason for hope. The same data that shows the gaps also shows the momentum:

- As of December 2024, 27 million women were monitoring their credit, marking a 42% increase from the previous year, signaling growing financial awareness.

- Female DEMAT account holders in India grew 4.2x from 6.67 million in 2021 to 27.71 million by 2024.

- Women-led startups recognized by DPIIT grew from 1,943 in 2017 to 17,405 in 2024 — an 800% increase. (DPIIT)

- Rural women now hold 42.2% of all bank accounts, reflecting growing financial autonomy outside metros.

Indian women are waking up. And when they do, they build wealth with remarkable discipline and intention.

This Women’s Day, We Choose Financial Courage

The theme of International Women’s Day 2026 is Accelerate Action. And no action accelerates a woman’s life quite like financial independence.

Not because money is everything. But because without it, so many other freedoms become inaccessible. The freedom to leave a bad marriage. The freedom to say no to a job that doesn’t respect you. The freedom to take care of your parents. The freedom to take a risk on your dream.

Financial freedom is not about being rich. It is about having enough options to make choices that align with your values — not your fear.

“Every informed choice brings us closer to the financial freedom we deserve.”— Prerna Rohilla, Founder — Mom, Money & Mindset

To every single mother who is doing it alone — you are not failing. You are doing the work of two people, and you deserve support, community, and financial tools built for your reality.

To every woman in a joint family who has never been included in the financial conversation — you have the right to ask. And the right to know.

To every woman living with her parents, waiting for her ‘real life’ to begin — your life is happening right now. And so is your opportunity to build wealth.

To every working woman who earns her own money but still doesn’t trust herself with it — the gap is not capability. It is confidence. And confidence is something we build together.

Happy Women’s Day. Now let’s get to work.

Sources: UN Women ‘Progress of the World’s Women’ Report | Tata AIA Survey | Finsafe India & Womantra Survey 2025 | Experian India Credit Awareness Report 2024 | MoSPI Women and Men in India 2024 | NFHS-5 (2019-21) | Outlook Money Survey 2025 | IndiaLends #WorkingStree Survey