Your child’s school teaches them the periodic table. They learn the Pythagorean theorem, the causes of the First World War, and how to conjugate verbs in three languages. They have homework on photosynthesis and projects on the water cycle.

But when they tap their phone to pay for a samosa — spending money they may not have properly accounted for — nobody taught them what just happened to their finances. Nobody explained the difference between spending and saving. Nobody showed them how interest compounds, how a budget works, or why the money in their piggy bank is quietly losing value to inflation.

This is not a small gap. It is a generational one. And in 2026, as India undergoes the most ambitious transformation of its education system in decades, this gap is becoming more urgent — not less.

India’s Education Revolution — What Is Actually Changing

To understand the opportunity, we first need to understand the transformation that is already underway.

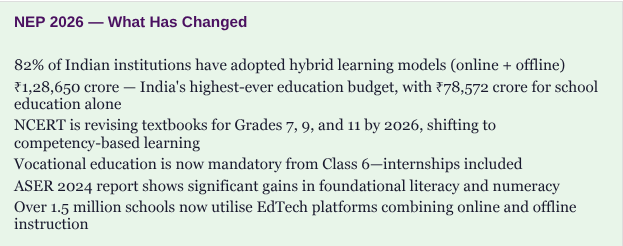

The National Education Policy 2020 is India’s most sweeping educational reform since independence. After decades of rote-learning and exam-obsessed schooling, NEP 2020 is fundamentally redesigning what — and how — Indian children learn. By 2026, its implementation has reached a critical inflection point.

The changes are real and significant. The old 10+2 structure has given way to a 5+3+3+4 model that better mirrors how children actually develop. Competency-based learning is replacing the memorise-and-reproduce approach in 67% of educational institutions. Vocational education is now mandatory from Class 6 onwards. AI literacy is being introduced from middle school. Critical thinking, collaboration, and creativity have been formally written into the curriculum framework.

These are not cosmetic changes. India is genuinely trying to prepare its 260 million students for a world that demands adaptability, critical thinking, and practical skills. The intent is admirable. The execution is accelerating.

And yet, in this ambitious redesign of what Indian children learn, one subject remains conspicuously, bafflingly absent.

“India is teaching children to code, to think critically, to collaborate across disciplines — but not how to manage the money they will earn from doing all of these things.”

The Subject No Indian School Teaches — And Why It Matters Most

Financial literacy is the ability to understand and effectively use financial concepts — budgeting, saving, investing, debt, insurance, and taxes. It is not a niche skill for finance professionals. It is the foundation of every adult decision a child will eventually make.

And India’s children are growing up without it.

The irony is staggering. We live in a country that built UPI — the world’s most advanced real-time payment system. India processed a record 21.63 billion UPI transactions in December 2025 alone, with 500 million unique users by early 2026. Our children aretapping phones, scanning QR codes, and making digital transactions before they have learned to read a bank statement.

This is not just a gap in knowledge — it is a gap with measurable consequences. Research from the RBI consistently shows that early financial education leads to better saving habits, lower debt accumulation, and greater long-term wealth. A 2025 study found that programs targeting financial education for children showed a 17% increase in household savings over two years. The returns on teaching money skills are extraordinary — and India is leaving them entirely on the table.

The Digital Paradox

Here is the paradox that should alarm every parent and policymaker: Indian children are the world’s most digitally active in financial transactions — and among the least financially literate.

A 2026 research study found that 48% of Indian students use UPI daily, and 43% use it several times per week. They are primarily spending on food, peer-to-peer transfers, and college activities. They know how to send money. They do not know why saving that money matters, what happens to it when it sits in a zero-interest account, or how to recognise a UPI scam — which the RBI flagged as doubling in 2025, with teenagers as the primary target.

We have given our children the car. We have not taught them to drive. And the road is getting faster.

Why NEP 2020, for All Its Ambition, Falls Short on Financial Literacy

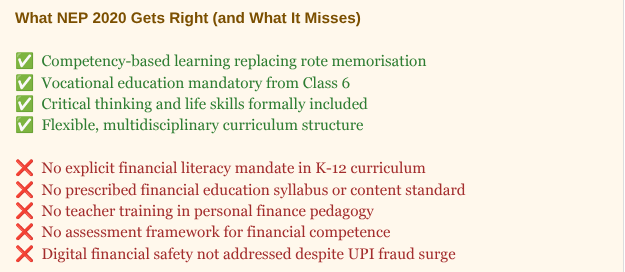

NEP 2020 is the most progressive educational framework India has produced. It talks about life skills. It talks about experiential learning and critical thinking. It introduces vocational education from Class 6.

But it does not explicitly mandate financial literacy as a core subject. There is no prescribed curriculum. No standardised content. No teacher training framework. No assessment rubric. The word ‘financial’ barely appears in the 66-page document, and when it does, it refers to the funding of educational institutions — not the financial education of children.

This is not a criticism of NEP — it is an invitation to complete it. The framework exists. The appetite for reform exists. The infrastructure — 14.72 lakh schools, 98 lakh teachers, 260 million students — exists. What is missing is the explicit recognition that financial literacy is not an extracurricular enrichment. It is a core life skill on par with literacy and numeracy.

The Countries That Got This Right

India is not the first country to face this gap — but it can learn from those who closed it.

The United Kingdom made financial literacy a mandatory part of the national curriculum in 2014. Today it is integrated into mathematics, PSHE (Personal, Social, Health and Economic Education), and citizenship from primary school.

Australia introduced financial literacy into its national curriculum in 2013 through ‘consumer and financial literacy.’ The results show measurable improvements in saving rates and debt management among young adults.

Singapore’s Ministry of Education integrates financial literacy across subjects from primary school, treating money management as a fundamental life skill alongside reading and writing.

Brazil, New Zealand, and South Africa have all introduced national financial literacy strategies for schools, with teacher training and standardised content.

India — with the world’s largest education system, one of its fastest-growing economies, and a youth population that will drive global growth for the next 30 years — has no equivalent programme. Yet.

What Financial Literacy in Schools Would Actually Look Like

When people hear ‘financial literacy in schools’, they imagine dense textbooks about stock markets and tax returns. That is not what this looks like in practice — or what it should look like.

Done well, financial education for children is engaging, experiential, and age-appropriate. Here is what it looks like at each stage:

Class 6 (Age 11-12) — Foundations

What money is, how it is earned, and what it represents in terms of human effort and time

The difference between needs and wants — and why this distinction is the bedrock of every financial decision

The 3-jar system: Spend, Save, Give — making money management tangible and visual

Opening a savings account and experiencing the act of saving toward a goal

Class 7 (Age 12-13) — Building

Budgeting: how to plan spending before it happens, not manage the aftermath

Banking basics: what a bank account does, how interest works, what a passbook shows

Inflation: why the samosa that cost ₹5 in 2010 costs ₹20 today — and what this means for idle savings

Introduction to digital payments: UPI safety, OTP security, and recognising scams

Class 8 (Age 13-14) — Advancing

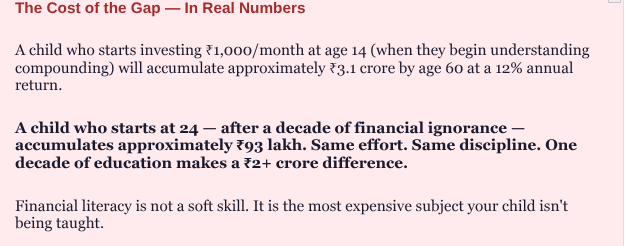

Compound interest: the single most powerful concept in personal finance, explained with real numbers

Introduction to investing: what a mutual fund is, what a SIP does, and why starting at 13 is genuinely life-changing

Entrepreneurship basics: from idea to small business, understanding revenue and costs

Credit and debt: how credit scores work, what EMIs actually cost, and how to avoid the debt trap

None of this requires a specialised teacher. None of it requires expensive infrastructure. All of it requires one thing: that someone — a parent, a teacher, a mentor — decides it is important enough to prioritise.

The Role of Parents — When Schools Don’t Fill the Gap, Families Must

Here is the uncomfortable truth: waiting for the school system to solve this problem is not a strategy. India’s education reforms are moving faster than ever before — but even the most optimistic timeline for a mandated national financial literacy curriculum is years away. Your child is in school right now. The gap is right now.

Research from the University of Cambridge shows that core money habits are formed by age seven. A separate analysis of financial outcomes found that children who discuss money with parents at least once a week score significantly higher on financial literacy assessments as adults. The home is not the backup classroom. For financial education, it is the primary one.

“Your child’s school may be teaching them to code, to think critically, and to collaborate — but the conversation about money that happens at your dinner table will shape their finances for the rest of their life.”— Prerna Rohilla, Mom Money & Mindset

This does not mean parents need to become financial experts. It means parents need to be willing to do three things:

Talk about money openly — without shame, without stress, and without the pretence that it is someone else’s domain

Give children real practice — pocket money, savings goals, small financial decisions — so that theory becomes experience

Seek out structured financial education resources that bridge the gap the school system has left open

What This Looks Like in Practice

The most powerful financial education tools are also the simplest. Letting your child pay for the groceries and count the change. Sitting with them at the end of the month and reviewing where the pocket money went. Asking them: if you had ₹1,000 and wanted it to grow, what would you do with it?

India’s economic trajectory makes this conversation urgent in a way that it was not even five years ago.

India will have the world’s largest working-age population by 2030 — over 600 million people aged 15-59. Their financial decisions will shape the Indian economy for decades.

India’s middle class is projected to expand from 300 million to 500 million by 2030. The majority of this growth will come from T2 and T3 cities — exactly where financial literacy access is lowest.

UPI has brought 500 million Indians into the digital financial ecosystem. Many of them — particularly young users — are transacting without the financial education to do so safely or wisely.

Women’s financial literacy in India remains under 20% — connected directly to lower digital access and an education system that historically treated financial agency as outside a woman’s domain.

These numbers are not abstract. They are the backdrop against which an entire generation of Indian children is growing up — children who will inherit an economy of extraordinary opportunity and extraordinary complexity. The question is whether we will prepare them for it.

What Needs to Happen — For Schools, Policymakers, and Parents

The solution operates at three levels simultaneously:

For Policymakers and the Education System

Financial literacy must be explicitly included in the NEP implementation framework — not as a suggested extracurricular activity but as a mandated component of the existing Life Skills curriculum from Class 6 onwards

NCERT should develop standardised, age-appropriate financial literacy content as part of the current textbook revision cycle for Grades 7, 9, and 11 — this is already underway for other subjects

Teacher training programmes (NISHTHA and others) should include a financial literacy pedagogy module — it does not require financial experts, only trained generalists

UPI digital safety — already a national security issue per RBI — should be formally included in digital literacy education for Class 7 and above

For Schools and Educators

Financial literacy content can be embedded within existing subjects without adding curriculum burden — maths classes for budgeting and compound interest, social studies for economic concepts, life skills for money management

Guest sessions with financial educators (parents, community members, professionals) can supplement classroom teaching at zero cost

Schools in T2 and T3 cities have a particular opportunity: their students will grow up in rapidly changing economic environments and need financial education the most

For Parents — Starting Today

Do not wait for the system to act. Your child needs this education now, and you are the most effective teacher they will ever have

Make money a normal topic at home — not a stressful one. One conversation a week at the dinner table is worth more than a semester of classroom instruction

Provide real-world financial experience: pocket money, savings goals, small budgeting decisions, banking visits

Seek out structured resources — books, workshops, and community programmes that give your child systematic financial education

The Conclusion — And the Invitation

India is building one of the most ambitious education systems in the world. NEP 2020 is a genuine, substantive reform that is changing what 260 million children learn and how they learn it. The people driving this transformation deserve credit for the scale of their ambition.

But ambition without financial literacy is incomplete. We are training children to succeed in the economy without teaching them to navigate it. We are handing them the tools of the 21st century without the instruction manual for the one tool they will use every single day of their adult lives.

The school system will catch up — eventually. Policy moves slowly. Curriculum reform takes years. Teacher training takes longer.

Your child cannot wait that long.

The most important financial classroom in India is not in a school. It is in your home, at your dinner table, in the conversations you choose to have and the experiences you create. That classroom is open right now. And the lesson — unlike most — has a return that compounds for life.

“Financial literacy is not about teaching children to be rich. It is about teaching them to be free — free to make choices, to take risks, to recover from mistakes, and to build a life of their own design.” — Prerna Rohilla, Mom Money & Mindset

Sources & References

National Education Policy 2020, Ministry of Education, Government of India (education.gov.in) | ASER 2024 Report, ASER Centre (asercentre.org) | UPI Statistics December 2025, NPCI (npci.org.in) | Financial Literacy Statistics 2026, CoinLaw | NEP 2025 Implementation Progress, Ministry of Education | NCFE National Financial Literacy Survey | RBI Financial Education Report 2025 (rbi.org.in) | Indian Education System Guide 2026 (eklavvya.com) | From Cash to Clicks: Student Perspectives on the UPI Revolution, IJIRT 2026 | EY Financial Inclusion Report India 2025 | University of Cambridge money habits research

1 thought on “India Is Rewriting Its Education System — But It Is Still Teaching Children Everything Except How to Manage Money”

Such a well written article, I must say …… But would want that it should reach pmo office …. So that this must be added in the curriculum in the near future.

Such a well written article, I must say …… But would want that it should reach pmo office …. So that this must be added in the curriculum in the near future.